Millimeter-Wave Automotive Radar Systems Market Report 2025: In-Depth Analysis of Growth Drivers, Technology Innovations, and Global Forecasts. Explore Key Trends, Regional Insights, and Strategic Opportunities Shaping the Industry.

- Executive Summary & Market Overview

- Key Technology Trends in Millimeter-Wave Automotive Radar Systems

- Competitive Landscape and Leading Players

- Market Growth Forecasts and Revenue Projections (2025–2030)

- Regional Analysis: Market Dynamics by Geography

- Future Outlook: Emerging Applications and Innovations

- Challenges, Risks, and Strategic Opportunities

- Sources & References

Executive Summary & Market Overview

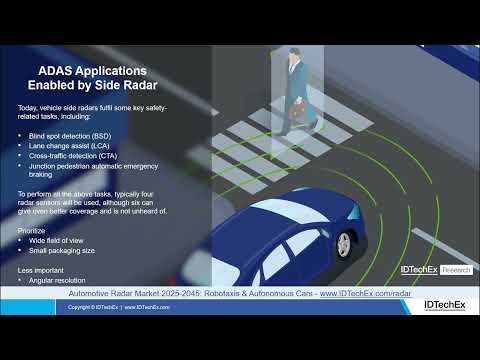

Millimeter-wave (mmWave) automotive radar systems are advanced sensing technologies that operate in the 24 GHz, 77 GHz, and 79 GHz frequency bands, enabling high-resolution detection of objects and precise measurement of distance, speed, and angle. These systems are integral to modern Advanced Driver Assistance Systems (ADAS) and autonomous driving features, providing critical data for functions such as adaptive cruise control, collision avoidance, blind-spot detection, and parking assistance.

In 2025, the global market for mmWave automotive radar systems is poised for robust growth, driven by the accelerating adoption of ADAS and the ongoing evolution toward higher levels of vehicle autonomy. Regulatory mandates in key automotive markets—including the European Union’s General Safety Regulation and similar initiatives in the United States and Asia—are compelling automakers to integrate radar-based safety features as standard equipment in new vehicles. This regulatory push, combined with rising consumer demand for enhanced safety and convenience, is fueling widespread deployment of mmWave radar sensors across vehicle segments.

According to recent market analyses, the global automotive radar market is projected to reach a value of over $10 billion by 2025, with mmWave radar systems accounting for a significant share due to their superior performance in adverse weather and low-visibility conditions compared to other sensor modalities such as cameras and lidar. The 77 GHz and 79 GHz bands, in particular, are seeing rapid adoption owing to their ability to deliver finer resolution and longer detection ranges, which are essential for next-generation ADAS and autonomous driving applications MarketsandMarkets.

- Key industry players—including Infineon Technologies AG, NXP Semiconductors, Texas Instruments, and Analog Devices—are investing heavily in the development of highly integrated, cost-effective mmWave radar chipsets and modules.

- Automotive OEMs are increasingly collaborating with radar technology providers to accelerate the integration of multi-mode radar systems capable of supporting both short-range and long-range sensing requirements.

- Emerging trends include the adoption of 4D imaging radar, which leverages mmWave technology to provide richer environmental data and enable more sophisticated perception algorithms for autonomous vehicles Strategy Analytics.

Overall, the 2025 outlook for mmWave automotive radar systems is characterized by rapid technological innovation, expanding regulatory requirements, and intensifying competition among semiconductor and automotive suppliers, all of which are shaping a dynamic and rapidly evolving market landscape.

Key Technology Trends in Millimeter-Wave Automotive Radar Systems

Millimeter-wave (mmWave) automotive radar systems are rapidly evolving, driven by the increasing demand for advanced driver-assistance systems (ADAS) and the progression toward fully autonomous vehicles. In 2025, several key technology trends are shaping the development and deployment of mmWave radar in the automotive sector.

- Higher Frequency Bands and Bandwidth Utilization: Automotive radar systems are increasingly leveraging the 77 GHz and 79 GHz frequency bands, which offer higher resolution and improved object detection capabilities compared to the legacy 24 GHz band. The expanded bandwidth in these higher frequencies enables finer range and velocity discrimination, critical for complex driving environments (Texas Instruments).

- Integration and Miniaturization: The trend toward system-on-chip (SoC) solutions is accelerating, with radar transceivers, digital signal processors, and microcontrollers being integrated into single compact packages. This integration reduces system size, cost, and power consumption, facilitating the adoption of radar in a broader range of vehicle models, including entry-level cars (NXP Semiconductors).

- Enhanced Signal Processing and AI: Advanced signal processing algorithms, often powered by artificial intelligence and machine learning, are enabling more accurate object classification, clutter reduction, and multi-target tracking. These improvements are essential for reliable operation in dense urban environments and adverse weather conditions (Infineon Technologies).

- Sensor Fusion and Networked Radar: There is a growing emphasis on fusing radar data with inputs from cameras, lidar, and ultrasonic sensors to create a comprehensive perception of the vehicle’s surroundings. Additionally, networked radar systems, where multiple radar units communicate and coordinate, are being explored to further enhance situational awareness and redundancy (Continental AG).

- Cost Reduction and Scalability: Advances in semiconductor manufacturing and packaging are driving down the cost of mmWave radar modules, making them accessible for mass-market vehicles. This democratization is expected to significantly increase the penetration rate of radar-based safety features by 2025 (Strategy Analytics).

These trends collectively position mmWave automotive radar as a cornerstone technology for next-generation vehicle safety and autonomy, with ongoing innovation expected to further expand its capabilities and market reach in 2025 and beyond.

Competitive Landscape and Leading Players

The competitive landscape of the millimeter-wave automotive radar systems market in 2025 is characterized by intense rivalry among established semiconductor manufacturers, automotive Tier 1 suppliers, and emerging technology firms. The market is driven by the accelerating adoption of advanced driver-assistance systems (ADAS) and the push toward higher levels of vehicle autonomy, which require robust, high-resolution sensing capabilities. Millimeter-wave radar, operating typically in the 24 GHz, 77 GHz, and 79 GHz bands, has become a critical technology for applications such as adaptive cruise control, collision avoidance, and blind-spot detection.

Key players dominating this space include Infineon Technologies AG, NXP Semiconductors N.V., Texas Instruments Incorporated, and Analog Devices, Inc.. These companies leverage their expertise in RF and mixed-signal integrated circuits to deliver highly integrated radar chipsets that offer improved range, resolution, and power efficiency. For instance, Infineon Technologies AG has expanded its portfolio with the RASIC™ family, supporting scalable radar architectures for both premium and mass-market vehicles.

Automotive Tier 1 suppliers such as Continental AG, Robert Bosch GmbH, DENSO Corporation, and Veoneer, Inc. play a pivotal role by integrating these radar chipsets into complete sensor modules and systems. These suppliers are increasingly focusing on multi-mode radar solutions that combine short-, medium-, and long-range detection in a single unit, addressing the needs of both urban and highway driving scenarios.

- Continental AG has announced next-generation radar sensors with enhanced object detection and classification, leveraging AI-based signal processing.

- Robert Bosch GmbH continues to expand its global production footprint, aiming to supply radar sensors for both passenger and commercial vehicles.

- NXP Semiconductors N.V. collaborates with automakers and Tier 1s to develop scalable radar platforms, supporting the transition to software-defined vehicles.

The market also sees competition from innovative startups and regional players, particularly in China and South Korea, who are leveraging cost advantages and local partnerships to gain market share. As the industry moves toward 4D imaging radar and sensor fusion, the competitive landscape is expected to further intensify, with ongoing investments in R&D and strategic alliances shaping the future of millimeter-wave automotive radar systems.

Market Growth Forecasts and Revenue Projections (2025–2030)

The market for millimeter-wave (mmWave) automotive radar systems is poised for robust growth in 2025, driven by accelerating adoption of advanced driver-assistance systems (ADAS) and the ongoing shift toward autonomous vehicles. According to projections by MarketsandMarkets, the global automotive radar market—of which mmWave systems (typically operating at 24 GHz, 77 GHz, and 79 GHz) are a critical segment—is expected to reach a value of approximately USD 7.5 billion in 2025, up from an estimated USD 5.8 billion in 2023. This growth is underpinned by regulatory mandates for safety features, such as automatic emergency braking and adaptive cruise control, which increasingly rely on high-frequency radar sensors for precise object detection and collision avoidance.

Regionally, Asia-Pacific is anticipated to lead the market in 2025, with China, Japan, and South Korea at the forefront of mmWave radar integration due to their strong automotive manufacturing bases and aggressive government safety regulations. Statista projects that the Asia-Pacific region will account for over 40% of global revenue in this segment. Europe and North America will also see significant growth, driven by premium vehicle manufacturers and the rapid rollout of Level 2 and Level 3 autonomous features.

From a technology perspective, 77 GHz and 79 GHz mmWave radar systems are expected to dominate new installations in 2025, as they offer higher resolution and longer detection ranges compared to legacy 24 GHz systems. This shift is reflected in the product roadmaps of leading suppliers such as Infineon Technologies AG and NXP Semiconductors, both of which are expanding their mmWave radar portfolios to meet OEM demand for multi-mode, multi-range radar modules.

Looking ahead, the compound annual growth rate (CAGR) for mmWave automotive radar systems is forecasted to exceed 12% between 2025 and 2030, with total market revenues projected to surpass USD 13 billion by the end of the decade (Market Research Future). This trajectory underscores the critical role of mmWave radar in enabling next-generation vehicle safety and autonomy.

Regional Analysis: Market Dynamics by Geography

The regional dynamics of the millimeter-wave automotive radar systems market in 2025 are shaped by varying levels of technological adoption, regulatory frameworks, and automotive industry maturity across key geographies. North America, Europe, and Asia-Pacific remain the primary markets, each exhibiting distinct growth drivers and challenges.

North America continues to lead in early adoption, propelled by stringent safety regulations and a robust ecosystem of automotive OEMs and technology suppliers. The United States, in particular, benefits from the National Highway Traffic Safety Administration’s (NHTSA) push for advanced driver-assistance systems (ADAS), which has accelerated the integration of 77 GHz radar modules in new vehicles. The presence of major players such as Texas Instruments and NXP Semiconductors further strengthens the region’s innovation pipeline.

Europe is characterized by a strong regulatory environment, with the European Union’s General Safety Regulation mandating advanced safety features, including autonomous emergency braking and lane-keeping assistance, in all new vehicles from July 2024. This has led to a surge in demand for high-resolution millimeter-wave radar systems, particularly among German automakers like Bosch and Continental AG. The region’s focus on reducing road fatalities and supporting the Vision Zero initiative is expected to sustain high growth rates through 2025.

- Germany: Dominates the European market due to its premium automotive sector and strong R&D investments.

- France and the UK: Show increasing adoption, driven by both regulatory compliance and consumer demand for safety features.

Asia-Pacific is the fastest-growing region, fueled by the rapid expansion of the automotive industry in China, Japan, and South Korea. China’s government incentives for smart vehicles and the proliferation of local radar module manufacturers, such as Hesai Technology, are accelerating market penetration. Japanese automakers, including Toyota and DENSO Corporation, are also investing heavily in millimeter-wave radar R&D to support both domestic and export markets.

Emerging markets in Southeast Asia and Latin America are expected to witness gradual adoption, primarily as global OEMs introduce radar-equipped models to comply with evolving safety standards. However, cost sensitivity and limited infrastructure may temper short-term growth in these regions.

Overall, regional market dynamics in 2025 will be shaped by a combination of regulatory mandates, OEM strategies, and consumer awareness, with Asia-Pacific poised for the highest growth, while North America and Europe maintain technological leadership and regulatory momentum.

Future Outlook: Emerging Applications and Innovations

The future outlook for millimeter-wave (mmWave) automotive radar systems in 2025 is marked by rapid innovation and the emergence of new applications that extend beyond traditional advanced driver-assistance systems (ADAS). As the automotive industry accelerates toward higher levels of vehicle autonomy, mmWave radar is poised to play a pivotal role due to its high resolution, robustness in adverse weather, and ability to detect objects at both short and long ranges.

One of the most significant emerging applications is the integration of mmWave radar with sensor fusion platforms, combining data from cameras, LiDAR, and ultrasonic sensors to create a comprehensive perception suite for autonomous vehicles. This multi-modal approach enhances object detection, classification, and tracking, particularly in complex urban environments where occlusions and unpredictable obstacles are common. Leading automotive suppliers such as Bosch Mobility and Continental AG are actively developing next-generation radar modules with higher channel counts and advanced signal processing capabilities to support these applications.

Another innovation on the horizon is the deployment of 4D imaging radar, which leverages mmWave technology to provide not only distance and speed but also precise elevation and azimuth information. This enables vehicles to better interpret their surroundings, distinguishing between stationary and moving objects, and even identifying vulnerable road users such as pedestrians and cyclists. Companies like Uhnder and Ainstein are at the forefront of commercializing 4D imaging radar solutions, with several OEMs planning pilot deployments in 2025.

- In-cabin monitoring: mmWave radar is being adapted for driver and occupant monitoring, detecting micro-movements and vital signs to enhance safety and comfort. This is particularly relevant for child presence detection and driver drowsiness alerts.

- Smart infrastructure: Integration with vehicle-to-everything (V2X) communications is enabling radar-equipped vehicles to interact with smart traffic systems, improving traffic flow and safety at intersections.

- Cost and miniaturization: Advances in semiconductor manufacturing, particularly with CMOS-based mmWave chips, are reducing costs and enabling more compact radar modules, facilitating mass adoption across vehicle segments.

According to Strategy Analytics, the global automotive radar market is expected to surpass $10 billion by 2025, with mmWave systems accounting for a growing share due to these technological advancements and expanding use cases.

Challenges, Risks, and Strategic Opportunities

Millimeter-wave (mmWave) automotive radar systems, operating typically in the 24 GHz, 77 GHz, and 79 GHz frequency bands, are pivotal for advanced driver-assistance systems (ADAS) and autonomous driving. However, the sector faces a complex landscape of challenges and risks, even as it presents significant strategic opportunities for stakeholders in 2025.

Challenges and Risks

- Electromagnetic Interference (EMI): The proliferation of mmWave radar units in vehicles increases the risk of mutual interference, especially in dense urban environments. This can degrade detection accuracy and reliability, posing safety concerns and necessitating advanced signal processing and coordination protocols (NXP Semiconductors).

- Cost and Integration Complexity: Integrating mmWave radar with other sensors (LiDAR, cameras) for sensor fusion is technically demanding and costly. The need for miniaturization, high-performance chipsets, and robust packaging to withstand automotive environments further escalates development and production costs (Infineon Technologies).

- Regulatory and Spectrum Allocation: Regulatory bodies worldwide are still harmonizing spectrum allocation for automotive radar, with regional differences in allowed frequency bands and power limits. This fragmentation complicates global product rollouts and increases compliance costs (International Telecommunication Union).

- Supply Chain Vulnerabilities: The mmWave radar market is sensitive to semiconductor supply chain disruptions, as seen during recent global chip shortages. This risk is exacerbated by the high demand for advanced process nodes and specialized packaging (Gartner).

Strategic Opportunities

- ADAS and Autonomous Vehicle Growth: The rapid adoption of ADAS and the push toward higher levels of vehicle autonomy are driving demand for high-resolution, all-weather radar systems. Companies investing in scalable, software-defined radar platforms are well-positioned to capture market share (Continental AG).

- Emergence of 4D Imaging Radar: Next-generation 4D imaging radar, which provides richer environmental data, is opening new use cases in urban navigation, vulnerable road user detection, and in-cabin monitoring (Analog Devices).

- Standardization and Ecosystem Collaboration: Industry-wide efforts to standardize interfaces, protocols, and testing methodologies can reduce development costs and accelerate time-to-market, benefiting both established players and new entrants (SAE International).

Sources & References

- MarketsandMarkets

- Infineon Technologies AG

- NXP Semiconductors

- Analog Devices

- Strategy Analytics

- Texas Instruments

- Robert Bosch GmbH

- Veoneer, Inc.

- Statista

- Market Research Future

- Bosch

- Hesai Technology

- Toyota

- Uhnder

- Ainstein

- International Telecommunication Union